WELCOME TO MIKE KAHN'S GOLF COURSE BUYER'S GUIDE (Original Free Copy)

NEW!

IT'S 2022 GOLF COURSE BUYER'S GUIDE

Remember, your first consultation is always complimentary.

Michael A Kahn, Golfmak, Inc. Always available:

Send me an email: mike@golfmak.com (I always reply)

FREE VERSION PUBLISHED EARLIER (NOW HISTORY)

THE COVID FACTOR HAS MADE GOLF THE 'DARLING' PASSTIME FOR PEOPLE SUFFERING FROM CABIN FEVER AFTER BEING SHUT IN FOR OVER A YEAR!

YOU NEED TO ESTABLISH YOUR MISSION. I MEAN DON'T LET PASSION CLOUD YOUR BUSINESS MIND!

The Golf Course Business has changed since my original guide published here in 2002

NOTE: If you plant to own a golf course in 2022 or beyond, be sure to talk to me before embarking on your mission. The golf business is a very different 'animal' than it was when this article was first written. For instance, financing is all but impossible in 2014 - unless the seller of a golf course is willing to be your banker. However, the good news is: I'm watching $5 million dollar golf courses being sold for barely $1 million. Let's talk. Your first consultation with me is complimentary.

2022 - NEW SERVICE: Let us help you write your business plan. Whether it's before you start looking, or you already have a golf course in your sites, We can help you focus on the things that will streamline you to success. Not only be a better operator, but if done right you'll reduce your personal energy output by eliminating all the mistakes we've already made over 60-years in golf course operations. Your business plan will (should) address everything from qualifying yourself financially to all the elements of running a golf course. You outline elements like: food service; greens maintenance; merchandising; employees and wages; cash flow forecasts; marketing plans; and several other areas. It will be a plan you will refer to often - and even adjust from time-to-time - over the years. Write me: mike@golfmak.com for a quote.

FREE CONSULTATION BY EMAIL.

IF YOU ARE READY TO BUY A GOLF COURSE CONTACT: MIKE@GOLFMAK.COM, or Write me: mike@golfmak.com

I will help you through the nine steps to buying a golf course:

- Qualify,

- Search,

- Identify,

- Contract,

- Diligence,

- Finance,

- Close,

- Transition, and

- Management.

2022 UPDATE: 8 years ago I said, "Man, we've seen some strange things in golf course activity! In recent years one of the 'largest' golf companies in the world handed the keys to the bank for three Florida golf courses - and just walked away! We learned later that one of the three, a private club in the Orlando market, closed its doors after the banker pulled the plug. Just about everywhere I look I'm seeing 'corporate-owned' golf courses floundering and financially crashing. On the other hand, I see many on-site owner-operator golf courses flourishing. Failed corporate golf courses are being brought up by individuals who are ready to roll up their sleeves. Stay tuned, as there are more deals coming!"

2022 UPDATE: Opportunity Knocking? Yes! There are great opportunities to take over failing community or neighborhood golf courses - but you'll have to be cash ready. For instance: take this 18-hole championship golf course, fully irrigated, with clubhouse, maintenance building, all equipment available for under $2 million. You could not replace this course designed by a famous architect for less than $8 million! Yes, it has a few minor issues, but the fairways, greens, bunkers, tee boxes are in very good condition. It has a strong membership who are dying to have a solid, caring owner to earn their loyalty and spending habits. I believe the right owner can rely on a return of 10% to 17% depending on various skills in this business.

MORE: A Bradenton, Florida area golf course sold recently for only $800,000. Not a junk golf course, this was an 18-hole, par-72 golf course in decent, but far from perfect condition. A great location too. The catch: It had absolutely no equipment, because all maintenance was outsourced. However, it would take only another $300,000, more or less, to acquire a mix of purchased and leased equipment. What a deal!

2022 (No dramatic changes) UPDATE: Most golf course sales over the years 200 through 2018, seem to be between the buyer and the bank. I can name about a dozen in a few seconds. The banks don't appear to make much sense, because they hold out for a high price for a time, usually at least a year, then give up and sell it for 10 to 20 cents. I've watched the banker's method (once they own the golf course): First they hire a management company to run the golf course. There are about a dozen of these companies who gladly take these easy-money management contracts. Then the banker orders an evaluation of the subject, which can be any number from a dollar to the national debt. They'll watch the course lose $7,000 to $15,000 a month until they scream, "Uncle!" and sell the course to the first person who writes a check.

I watched a bank hold out for $1.8 million for about a year, then took $900,000 for a Wilmington, NC golf course.

I watched another banker turn down a cash offer for $2.1 million for an Orlando area course, then took $800,000 a year later.

Another Orlando area country club sold for barely over $3 million when a year earlier the bank wanted $4 million.

I WANT TO PREPARE YOU: Some of our readers (millions to date) believe this article is designed to discourage them from owning a golf course. In fact, what I am trying to do is support your resolve to do it, but do it right! I want you to be prepared for the costs, the detailed diligence, the financing red tape, and the transition process involved in buying and financing a golf course. All that tedious work really helps you when you take over the golf course. You'll have a great head-start, because you'll know every nook and cranny of the place.

'DOWN-HOME' MANAGEMENT STYLE NEEDED (corny, but true): In our experience most of these bargain-priced golf courses desperately need on-site, hands-on ownership. They need owners willing to shake hands and greet golfers at the door. They need more attention to bunker conditions, putting surfaces, and clean washrooms. They need a sincere effort from ownership to make them feel welcome and appreciated - the key to creating long-term player loyalty. Today, virtually every golf course with that kind of ownership is flourishing and making money. I simply hope to prepare you so you can own your own golf course - and be successful.

If you're ready,

READ ON!

TOPICS

2- YOUR COMMITMENT. ARE YOU READY TO OPERATE A GOLF COURSE?

3- ESTABLISHING WHAT YOU CAN AFFORD. ITEM #8 BELOW IS A 'WAKE-UP' CALL FOR MANY!

5- THE CONTRACT - PURCHASE AND SALE

6- 250 ITEM DILIGENCE CHECKLIST. A GOLF COURSE IS MADE UP OF MANY DETAILS

7- DILIGENCE COSTS AND CLOSING COSTS. FEW ARE TRULY PREPARED.

8- CASH NEEDS FOLLOWING POSSESSION DATE

Before you decide to own a golf course, it is important to remember that a golf course is like a 3-week old baby - it needs virtually 24/7 care. Assuming you love the game, I assume you're prepared to work long hours - often 7-days a week. I assume you'll be willing to give up long-weekend holidays because that's when you can make hay!. You realize, unlike a baby, a golf course never grows out of dependency. In fact, as a golf course ages its care and needs become even greater. In this highly competitive market, it is even more important for you to be a hands-on owner!

WHY DO YOU WANT TO OWN A GOLF COURSE?

The first thing you need to write down before entering golf course ownership is your mission. You should write down exactly what it is you want to gain by owning a golf course. Here are a few reasons a person or group may wish to own a golf course:

1. Pride of ownership

2. Love the game of golf

3. To change vocations

4. To run the operation like a business, and to make a profit

In the opinion of the writer, me, the fourth reason is the only reason a person or group should invest in a golf course. The first three reasons are, in my opinion, a scenario for financial disaster. If any of the first three reasons are yours, convert your thinking to number four! Reason number four can satisfy the first three reasons (round and round we go), but if you make any decisions based on the first three, the word 'business' is quickly eliminated. I've seen the same mistake over and over: Financial disasters when the opportunity was so promising!

THE MISSION STATEMENT

The first thing you need to understand is that the golf course business is as competitive as any business (even more competitive in the economy of 2012). Attracting loyal golf play at a reasonable price so you can make a reasonable profit must be the cornerstone of your mission. April 2012: You must learn to market your golf course. I mean LEARN how to REALLY market your golf course.

To be competitive, a golf course needs good greens, good fairways, good tees, and properly groomed bunkers. It needs to be a reasonable test of golfing skill. It must be competitively priced. If your target is located in a highly competitive neighborhood, the only advantage you can have over competitors may be course conditions and service. You must be committed to providing superlative service and maintaining spotlessly clean surroundings as your most important operational rule. "You must be prepared to fix problems immediately." Without that kind of commitment the golf community will abandon you. April 2012: Take a real good look around. So few golf course owners review their properties - like: Are the comfort stations and rain shelters clean?

Therefore, the mission statement should read, "My efforts as a golf course owner will be to provide a reasonable challenge, with good greens, good fairways, good tees, good bunkers, clean surroundings and the best service - all at a reasonable price. "I promise to have all the hazards clearly marked at all times!" April 2012: When I see hazard stakes missing, un-groomed bunkers on Sundays, or "soft cups (unchanged for several days)" I'm seeing a golf course business destined to fail.

MAIN OBSTACLES TO YOUR MISSION STATEMENT

1. Nature: Weather, pests, environmental issues

2. Service Challenges: Employees (low paid service personnel are difficult to motivate)

3. Competition: Every time a new golf course opens for play, it takes play away from you

4. Redundancy: Modern golf equipment has rendered many golf courses obsolete (under 6,500 yards = noncompetitive by tour standards). Well... that's changed somewhat in 2012. Actually they're building golf courses too long. Most golfers over 40-years of age cannot reach a 420-yard par-4. Sure, the pros do, but many of them hit a thousand balls a week. Actually, it's kind of dumb. They have to marquee the course at 7000-yards, but set the tees at 6200 or most players won't finish on the same day. Waste about 25-acres to stretch out 800-yards!

LET'S BRIEFLY REVIEW THESE ISSUES

Nature: Weather, pests, environmental issues: Obviously, you have no control over weather. A drought or a rainy period can ruin fairways and greens. You're faced with a barrage of pests like mole crickets, nematodes, fungus diseases, varmints and all sorts of natural attacks. Meanwhile, irrigation restrictions, chemical bans and restrictions can tie your hands to providing treatments and cures to save your golf course. For instance, a wall-to-wall mole cricket treatment costs $35,000 or more and only lasts six months (Mole crickets are one of the most destructive turf creatures anywhere. Failure to treat will devastate a golf course and could cost you $ hundreds of thousands in lost revenue and recovery maintenance. To learn about this creature, go to Internet site: http://www.ces.uga.edu/pubcd/L414.htm).

Service Challenges: Employees (low paid service personnel are difficult to motivate): All but your superintendent, golf professional and kitchen manager are among the lowest paid employees anywhere in the workforce. You'll be constantly turning over and training personnel. Grounds maintenance staffing can be particularly difficult to retain, because the pay is low, and their workday starts as early as 5:AM. You’ll also find it difficult to motivate low-paid service employees to keep them showing up for work – full of enthusiasm. April 2012: In my experience, paying the highest wages in the marketplace is good marketing! You get better workers, better employee loyalty, and ultimately a better product. If you pride yourself on how little you pay your people (you know who you are), you are bound to fail in the golf business.

Competition: Every time a new golf course opens for play, it takes play away from you: Competition from new golf courses grows every year. Add to that all the private golf clubs that have opened their courses to public play. Most studies on the growth golf in the USA indicate stagnant player participation since 1990, yet over 3,000 golf courses have been built since then. That simply means fewer golfers per golf course. UPDATE April 2012: Thank goodness they've come to their senses! New golf course development has slowed to a trickle. That's why I say,"This is the best time in history to buy a golf course!"

Redundancy is a recent 'sudden realization' phenomenon in the golf course business. Many golf courses more than 10 years old are so challenged by 300+ yard drives that they need to be retooled or redesigned to provide the same test level they did when they first opened. A leading golf course architect recently reported that he has moved his fairway 'guide bunkers' from 600 feet to over 850 feet from the tee boxes to provide the same relative test of ten years ago. UPDATE April 2012: I'm observing another return to sanity in this business. The golf course industry is learning that the sub-6,500 yard golf courses are more enjoyable and often more profitable.

Modern golf equipment (clubs and balls) has rendered many golf courses obsolete (noncompetitive): "Golfers move around like a school of fish, usually attracted to the newer golf courses. Remember Kahn's rule: New golf courses don't create new golfers, they take golfers from other golf courses. You'll want to take a hard look at the golf course in your sites in terms of redundancy. Look carefully to see if the layout can be retooled to meet the 2005+ golf player demands. It's almost all in length (*it really isn't to the average golfer, but that's another story). It might be that if you can't add a few hundred yards to the score card sometime down the road, you may be looking at an out-of-date golf course.

*"I always laugh when I look at the back, 7,000+ yard tee boxes (usually gold or black markers). The grass is always absolutely perfect, because nobody goes there. Even though the course is marketed as a 7,000+ yard test, 95%, no 99%, of players play ahead of the back tees - either the white or forward tees. The middle and forward tees are usually under 6,500 yards. That extra real estate needed for the extra 400 yards (about 20 acres) is the dumbest waste of real estate you can imagine! I'm sure there's a formula that will show that Tiger's 300+ drives have added more than a few dollars to the cost of a round of golf." UPDATE April 2012: I would enjoy your comments on this one. If Tiger woods causes older golf courses to become redundant and forced new golf courses to be tougher and longer, has he really helped the game? Write me with your comments: mike@golfmak.com.

It is extremely important that your commitment to managing the golf course you plan to own is sincere all the way. You are about to become a multifaceted 8-in-one businessperson:

1. You'll be in the food and beverage (restaurant) business. UPDATE April 2012: I say keep it simple. Read why weddings make me cry. Food and beverage can be highly profitable, but don't try to be a restaurant, because you cannot and will never compete with Outback Steakhouse. I made a ton of money in food and beverage by sticking to a simple menu - burgers, fries, grilled cheese, egg salad etc. Meanwhile, get used to the government in your face (health, fire and safety, etc.). Try to be in the "PURE" golf business.

2. You're about to become a retail merchandiser (golf/tennis pro shop). UPDATE April 2012: We had a saying back a few years, "The banker won't take golf clubs, golf shirts, or golf shoes as mortgage payments!" Too many merchandisers are paying taxes for profits when they are still on the shelves. Learn how to merchandise. Learn how to manage mark downs. Inventory on the shelves is like ice in summer - shrinking in value every minute.

3. You'll likely become a practice range operator. UPDATE April 2012: The practice range issue is a major bug with me. Too many operators give the range little more than lip service. Clean, quality range balls and decent practice turf is a must. I ran a range for almost 30-years. Man, we made good money every year!

4. You'll need to become a psychologist and Membership Director (managing a membership - believe me, it's an Art!). UPDATE April 2012: Memberships are declining almost everywhere in the country. You want to hold them as best you can, but you cannot let your members dictate policy. I have a horror story I will be glad to discuss with anyone directly. It's a case where membership was running the business under constant threat. Best is to call me: 941-739-3990.

5. You will become a farmer (turf manager). UPDATE April 2012: Turf conditions are Paramount! You need to know your turf issues as well as your superintendent. The best service in the world won't mean a 'hill of beans' if your greens are poor. I mean, you want those people on your golf course so you can give them great service!

6. You will become an advertising and marketing person (you better learn how to write and place an ad - marketing is crucial in today's golf business survival game). UPDATE April 2012: Developing marketing skills is the most important single function you will have in today's golf business marketplace. Become a net worker. Learn to use Facebook and Twitter. Build interaction between you and your customers.

7. You need to be an accountant - watching your revenue activity every day. Review and understand the balance sheet often. Following trends is very important as you watch your golf course perform financially. UPDATE April 2012: Your Point of Sale (POS) and Accounting Program is vital for monitoring your golf course business today. A good system will be highly user friendly and should make you money. The best systems can integrate with your accounting software and connected with the Internet for 24/7 online tee sheet availability. There are now several very good systems out there, some better suited to daily fee courses, some for private clubs. Write me for the POS systems I believe may be best suited to your golf course: mike@golfmak.com.

8. Personnel or Human Resources manager. You need to learn how to manage employees - many of whom are on the lowest end of the pay scale. Turnover is frequent. Theft, tardiness, performance indifference are often prevalent. UPDATE April 2012: If you have more than 10 employees, you need a Professional Employment Organization (PEO). Believe me, employee issues and your protection is vitally important in this ambulance-chasing and changing employee environment.

Weekends off? Not if you're aiming for success. Not too many golf course owners are fishermen!

You need to find out what sort of golf course you can afford to buy.

Immediately put together a financial statement that bankers can verify. Even if you pay cash for the chosen property, you'll still need to fill out hundreds of credit applications for your suppliers. Supply sources for Titleist golf balls, Toro machinery, etc. will want financial information on you to establish your credit (unless you plan to do business on COD, which means you've got more money than brains and don't need to read this stuff). If you're hesitant to tell the world your financial affairs, you'll create a roadblock to your golf course operations. You'll need everything from irrigation repair parts to ground beef from many different suppliers and services to run a golf course. Without established credit, you won't be able to operate properly. UPDATE April 2012: Don't be surprised if many suppliers put you on COD until you have established your credit. Obviously, until you establish trade credit you will need additional operating capital to pay for stuff like Coke and repair parts.

BE HONEST WITH YOURSELF! Anyway, you need to identify exactly what cash you have available as your down payment. You also need plenty of operating capital to address the hundreds of surprises you'll encounter during your first six months of ownership. Believe me, no matter how careful your diligence, you will encounter unforeseen expenses. UPDATE April 2012: This oversight is the number-one mistake first-time golf course buyers make. Many are in financial trouble six months into ownership.

Here's the Mike Kahn formula:

"In the 2012 golf course marketplace you need to be sure you have plenty of operating capital available immediately after the close. We try to warn golf course buyers to avoid highly leveraged acquisitions where they can be wiped out in one rainy month. I recommend planning 70% of your cash for the purchase or your down payment including closing costs and keep aside 30% for operating capital (if you borrow the banker wants that too). Remember the older the golf course, the more you will need available in capital (or reserves).

What I'm saying in 2012 is that you'll need $3.5 million to safely acquire a $3 million dollar golf course in 2012. That's $3 million to buy the course, up to $200,000 in costs, plus $300,000 in ready capital the day you take possession.

CASH/EQUITY AVAILABLE: $1,300,000 - UPDATE April 2012: You can buy a $1 million dollar golf course.

DOWN PAYMENT AMOUNT: $700,000 - UPDATE April 2012: You might pull this off with Seller Financing.

CLOSING COSTS: $300,000 - UPDATE April 2012: Should be close, but less if you have a Seller Financed deal.

OPERATING RESERVES: $300,000 - UPDATE April 2012: Depends on the property and the quality of your diligence. However, I recommend at least that much - always.

Forget this passage from 2004! The $700,000 down payment (now $1 million) illustrated above can buy a golf course from $1,000,000 (full price) to as high as $10 million at 90% financing. Of course, your down payment depends on factors comfortable to a lender and to your personal financial goals (helping to determine the appropriate down payment is one of Mike Kahn's client services). UPDATE April 2012: I help buyers and sellers work out a seller finance deal. You still need to treat the seller like a banker. It's best that you qualify yourself to be the borrower - even if the seller is your banker. To start the process, click this link: Finance a Golf Course.

Diligence expenses and closing costs are stated above at $300,000, but you could be paying up to $200,000 or more in sales commissions alone. By requiring financing expect costs for legal expenses, an independent feasibility study, environmental reports, a third-party business plan, an updated survey, an updated appraisal and other expenses that can run the ‘closing cost’ tab up sharply (we address closing and transition expenses later). UPDATE April 2012: If you are using Seller Financing, many of the above expenses will not be needed.

"WARNING! Golf courses more than ten years old can become 'money pits' for inexperienced buyers (remember the movie?). In Mike Kahn's opinion, a golf course ages ten years to one in human terms. Therefore, a ten-year-old golf course may have the health equivalent of an average 100-year-old man (wading through all these issues is what Mike Kahn does in his diligence work for his clients). For instance, the average life span of an irrigation system is between 15 and 20 years. An irrigation system installed before 1995 is likely redundant in 2012. Sure, it still works, but the impeller shaft will likely break within ten years of the original installation – a $10,000 to $35,000 repair job!" UPDATE April 2012: Replacing old irrigation systems with fully automatic systems (up to $1 million or more) might actually pay for themselves almost immediately. With fewer new golf course under construction, irrigation companies are providing excellent financing to help older courses update their systems just to remain in business. Carrying costs might be offset by operational savings and better playing conditions (better business).

SO, YOU'VE GOT A MISSION STATEMENT. YOU'VE GOT THE MONEY. YOU'VE BEGUN YOUR SEARCH

SELECTING A PROPERTY. WHERE DO I LOOK?

To be blunt, you need to be prepared to relocate if you are truly serious about owning and operating your own golf course. Amazingly, many of our clients want to own a golf course within a few miles from home. I explain that there's only about 17,000 golf courses in the United States. That's a small number when you figure the country has over 300,000 restaurants. What I'm saying is that if your sticking to business (choice four above) you'll have to go where the best opportunity is located. There are three basic regional locations you might consider (these are my terms):

1) The Freeze Zone

2) The Shoulder Zone

3) The Tropics. Lets sort these out:

Freeze Zone: Where the ground is frozen over for a long enough period that you need to drain your irrigation lines like Saginaw, Michigan, Milwaukee, Wisconsin, Toronto, Ontario, or Butte, Montana. Most golf seasons in these areas are about 200 days. Golf course buyers usually don't favor Freeze Zone golf courses because of the cold winter weather. However, if they're run right, you get to spend your winters in Florida. UPDATE April 2012: Many of the best opportunities are where it snows!

Shoulder Zone: The ground never really freezes beyond a few inches, but the midwinter months all but close you down, and the summers are as hot as Florida. You'll find courses like that in places like Virginia Beach, Virginia, Amarillo, Texas, or Nashville, Tennessee. A golf course in, say, Asheboro, North Carolina will have two comfortable periods we call the shoulder seasons - April, May and June, then September, October and November. The summer months are generally oppressively hot and humid, and the December through March months can get cold. Most of these courses never close except for the occasional snow cover. UPDATE April 2012: Be careful buying golf courses in this area.

Tropic Zone: You’re in business all year around, but those summer months are ever so hot. Consider places like Phoenix, Arizona, Fort Lauderdale, Florida or Corpus Christi, Texas. For instance, a golf course in Sarasota, Florida operates 365 days a year. The main revenue season runs from about January 10 through April 30 (or Easter). Either side of those days, it's a very competitive market, as the tourists have all gone north. Enduring 90+ temperatures every day from mid June to the end of October, some courses drop fees to as low as $10.00, including a cart to keep up some cash flow. UPDATE April 2012: In my opinion, June, July 2012 is the best time in history to buy a Florida, Texas, Arizona, or California golf course. Available for pennies on the dollar, I predict a spike in golf course prices in the next three years (Canadian dollar at Par is great for Florida and Arizona golf courses.

NOTHING WRONG WITH A FREEZE ZONE GOLF COURSE!

Too many prospective golf course buyers turn their noses up when presented with freeze zone golf courses (like Chicago). However, I've operated golf courses in both regions and in between. Golf courses in Chicago, Detroit, and Toronto (Canada) are extremely profitable, because of their short seasons and higher fees. I point out to buyers that in the peak season in Chicago, like July and August, they have several more hours of prime-time tee times (up to 10-hours) to sell than a course in Florida in February (6-hours maximum). Meanwhile, every November, freeze zone golf courses drains their irrigation lines and close right down. Florida golf courses have to keep up maintenance 12 months of the year - with those tropical grasses growing like mad!

SO, YOU'VE MADE UP YOUR MIND

You can put the word out to brokers that you are looking to buy a golf course, and you will get all kinds of deals from Alaska to Argentina. However, there are a few excellent golf course brokers out there who know the business and can steer you toward courses that fit your criteria. Call me, Mike Kahn, Golf Course Sales at First Tampa Financial Group: 941-739-3990 if you want over 50-years of golf course business experience working for you. UPDATE April 2012: If you want me to work for you, please call: 941-739-3990, or email: mike@golfmak.com

THE LETTER OF INTENT (OR MEMORANDUM OF UNDERSTANDING)

You might want to establish an understanding of the deal before you write the contract to buy the golf course in your sites. The intent of both parties (buyer and seller) can be established with a letter of intent (LOI). Usually non-binding in terms of a purchase or sale on either party, the document sets out the understanding between the two. In essence the buyer is asking what is exactly for sale, what's the price, what comes with it, etc. I often consider the LOI as important to the process as the purchase contract. Although a letter of intent may contain the words, 'non-binding' it still can be an important document in the deal if it contains intentional falsehoods from either party. We have a few one-page LOI boilers on file, but as time goes by, they are becoming more and more detailed - thanks to the attorneys, I guess. UPDATE April 2012: Go directly to contract! The LOI has been highly misused and has often been accused of 'hot dogging' sellers. With financing tougher today, and the bargains that are out there, I often recommend going straight to a contract. You'll know fairly quickly into your diligence whether you really wish to own a property. You'll also save on legal costs, as a letter of intent may cost you unnecessary legal expenses. I also believe the intent of the two - buyer and seller - can be verbal provided a contract is presented all but immediately.

When I'm part of the buyer's diligence team, I can sit in and help the buyer's attorney prepare the contract or letter of intent if that is the strategy. It is important that, as the buyer, you don't represent deeds or actions that the seller could throw back at you. With lawsuits running rampant, a seller could charge you with tying up his property, or worse, that you let out secrets about his property that seller considered proprietary. CYA all the way! UPDATE April 2012: Today, in many cases, a letter of intent may be more a waste of time and money.

"I have participated in the writing of several golf course purchase contracts. As a golf course buyer, having Mike Kahn at the table is like having a general from the apposition army assisting your strategy. I sit with the buyer and the attorney providing my experience to help draft the document so as many protections are in place for the buyer as possible. Let's face it. The seller's interests are the same as yours. He wants the best deal too! However, the seller knows things you've got to find out for yourself. Business is business!" UPDATE April 2012: There are many deferred issues you simply cannot see. I can be like your drug sniffing dog. I will not knowingly withhold information that you should have in your decision process. I know brokers who don't want me around, because they know I will not withhold information from buyers.

The offer to purchase a golf course property can be up to 100 pages in length (attorneys need the work). However, with so many licenses, permits, easements, contracts, etc., the contract needs to be as specific as possible. Every piece of equipment, every inventory item to be included in the price needs to be clearly spelled out. Don't forget the finance contingency. If a lender won't finance the golf course, you cannot buy it. Make sure you can get 100% of your earnest money back if you can't get financed. The earnest money deposit must be clearly defined and fully protected in case the property fails your diligence or your finance request. Buyer and Seller will select a mutually agreeable arms-length place to hold the deposit.

There's one clause I insist should be in the offer of purchase. I will reveal it to you by Email. Just click: mike@golfmak.com and ask the question.

HOW MUCH SHOULD I OFFER?

You need only to make an offer that addresses the real value of the property, your interests, and your financial capabilities (I can help you determine that). UPDATE April 2012: Banks and lenders lend on golf courses based on the ability of the business to repay the loan. If a golf course makes no money, it may be all but worthless in the eyes of a lender. Many golf course sellers in 2012 are taking a financial bath, as competition has been eating up profits of late. Sometimes upside potential can be un-quantify able and even unattainable. IN 2012 I BELIEVE YOU NEED TO CONDUCT A FULL FEASIBILITY STUDY FOR THE/A SUBJECT GOLF COURSE, BECAUSE SO MUCH HAS CHANGED SINCE THE COURSE WAS CREATED.

Don't waste your time and money pursuing a deal that doesn't make sense. In my opinion, if a golf course isn't making money it's not worth anything. Walk away from outrageous deals, no matter what they say about upside. Stick to a safe formula based on multiples of earnings, or the results of your own feasibility study. Don't pay over 10 time earnings, unless it is a brand new golf course and it passes your feasibility study! If you're paying a multiple of earnings I'm talking reliable earnings over the past five years. Even those earnings can be misleading if maintenance has been lax over the same period. Of course, that's where I come in. I can provide an opinion on what the real earnings are for a golf course by studying their revenues, rounds and expenses and matching that information with the condition of the property. UPDATE April 2012: I watched a buyer spend money and time chasing a deal that was all but impossible. Don't kid yourself! To own a golf course you must be able to afford it! Dreaming about the no-money down golf course will waste your time and everybody else involved.

To be sure, operational standards remain pretty comparable in shared golf course neighborhoods - subject to adjustments. I can usually learn by what the subject shows in maintenance expenses whether a deferred maintenance situation may be the reason for higher earnings - which may then be false. I can form an opinion, because I've studied cash flows from hundreds of golf courses all over North America. Matching financial activity with a physical inspection can reveal the subject's 'real' character. Remember, I was once an owner!

If you engage Mike Kahn, First Tampa Financial Group, as your exclusive Buyer’s Broker, I will help you decide upon a suitable golf course property. That's my business. UPDATE April 2012: Every one of my buyers is enjoying their golf course ownership. UPDATE 2013: Sorry to say that a couple of my buyers have either failed or sold and moved on. One just could not develop the proper bedside manner to deal with his leagues and members. It was a take-it-or-leave-it owner behavior that eventually lead to an exodus of members to other courses. With falling revenues the banker closed in and put him out on the street. Another owner sold and moved on after finding the task just too demanding. Those things happen.

HOW MUCH SHOULD YOU DEPOSIT WITH YOUR OFFER?

If your attorney is competent, you can make a stronger impact on the seller by putting up a eye-opening deposit without risking it. The key is how you write the contract to be sure you get it all back if you decide not to buy the property. However, you'll get a higher degree of cooperation from the seller if he sees you've put serious money behind your offer.

AM I THE FIRST ONE?

You're not likely to be the first ‘new’ owner of the golf course you buy. Like buying a used car, your getting a property that is in a condition reflecting how it has been used and cared for. You want to be sure you're not buying a money pit. There are a few telltale areas that you can observe to quickly learn whether the place has been properly maintained. I look at sand traps, edges of cart paths, sniff the water in the ball washers, and observe the comfort stations, etc., where neglect will be most obvious. I rub a finger along the reels on the fairway mowers, and take a peek into the pump house. If a golf course is more than three years old, it should already be on the second generation of specific maintenance machinery. Greens mowers, fairway mowers, trap rakes, etc. are only good for a number of working hours before they are beyond economical use (depending on whether it's a snow belt course, a tropical course, or somewhere in-between). Daily use machinery with more than 2,500 hours logged will be an indication that the seller has been cutting corners in the maintenance program. One of the best sources of information about the subject course's maintenance practices can be the assistant superintendent (not the head guy). A laid back conversation with this person can reveal an unreliable irrigation system, a worn out tractor, or expensive ongoing diseases or pest issues. Sometimes the superintendent won't tell you these things under orders from the seller. Dialogue is very important in the diligence process. A talk with a key club member, the starter, a ranger, or an assistant pro will alert you to problems the seller would rather you didn't know. Most of the bits of information you gather is normal wear-and-tear stuff and should be expected (not to be of a deal-killing nature). However, much of this information prepares you for the cash you'll need available after the change of ownership.

Remember, the older the course, the more deferred.

A true golf course buyer's diligence checklist should contain up to 250 separate items, with a couple of hundred more sub-issues. Every item needs to be taken seriously. Permitting, licensing, environmental issues, transferable leases, personnel contracts, supplier lists, available operational records, member lists, are among the headliners, but hundreds of smaller details can help the buyer avoid mistakes. This is where engaging the kind of experience I have at First Tampa Financial Group can help you in the decision processes.

Everything must check out. Remember that a golf course is an ongoing business. You don't want your power shut off, your phones turned off, your bar or kitchen closed down the day you take over. Different states, provinces and counties have different rules about health issues, environmental issues, etc. Don't take any person's word for anything. Get all documents and permits verified in writing - with copies in your hands! Minor diligence oversights can wind up as financial disasters. Beware: Verbal assurances from public officials can be fatal. Get the documents!

As a First Tampa Financial Group client, you get our 250-point diligence worksheet. If you check all these items properly, you’ll likely be pretty confident with what you’re buying.

IRRIGATION AND DRAINAGE

The two essentials for every golf course on the planet are irrigation and drainage. You must be absolutely sure you have adequate irrigation forever. UPDATE April 2012: Especially today!

IRRIGATION AVAILABILITY

Demands can be anywhere from 200,000 to 500,000 gallons for the daily irrigation needs of an 18-hole golf course. You must check the irrigation permits to be sure you have an adequate water source to irrigate under normal conditions. I say normal, because every neighborhood has contingencies in case of sever drought conditions. When droughts occur, the first cut will often be the local golf course. Meanwhile, irrigation permits are usually renewable, so you should check the renewal dates. Also see if there are any clauses that could cause you to lose the water altogether. Another irrigation source is waste water, or effluent - often referred to as 'gray' water. UPDATE April 2012: My how things have changed. In the early days of gray water irrigation, cities delivered waste water to golf courses for free. Lately, there's been a charge for effluent use in most cases. I've seen quotes like 10-cents per 1,000 gallons. Therefore a 400,000 overnight irrigation cycle will cost $40.00. Remember that is $40.00 more than the good ole' free water. A Florida golf course saw their irrigation costs go up over $15,000 when the county ordered them to use effluent, then charged them for it.

Effluent is the resulting waste water from community sewage treatment plants. Every community needs to get rid of their effluent safely, and there's no better place to dump it than on a golf course. If the community targets your course as a disposal site, you're likely to be obliged to accept it. Not only are you to accept effluent for irrigation, most communities make you pay to get it to your property. Then they charge you to use it!

Some irrigation permits are annual, some may be good for up to 20 years or more. Don't assume anything. Review the permits! UPDATE April 2012: Many irrigation water permits require monthly reports of daily irrigation water consumption.

THE IRRIGATION SYSTEM

You need to study the irrigation system carefully (I do that). Any golf course older than 10 years will have a system that has used up two thirds of its normal worry-free operational life. Not only are 10-year-old irrigation systems near redundancy, they maybe highly inefficient compared to the latest systems. Therefore, sometime in the next five years the system at your subject may need a complete overhaul - up to a $1 million dollar capital expense for an 18 hole golf course.

UPDATE April 2012: There are basically three types of irrigation systems: Manual, Semi-automatic, and Fully Automatic. Systems may be described as center line, twin-track, or wall-to-wall (tree-line-to-tree-line).

Manual Systems have no permanent in-ground heads. Each sprinkler head has to be plugged into the socket by hand. The manual sprinkler heads are moved in a leap frog manner through the course. Any manual system still operating will be up to 30-years old or more.

Semi-automatic Systems include individual in-ground pop-up heads that are controlled by stations located around the course (you've seen the green metal boxes out there). Sets of heads can be operated by each controller (station) using timers. Pop-up heads are activated either by electric solenoids, or by separate hydraulic pressure lines. Most of these systems will be ten or more years old.

Fully Automatic Systems can be operated by radio from hand held controllers or smart phones - capable of isolating single heads or any series of heads. The controllers are radio receivers in boxes located about the golf course. Most recent systems are fully automatic. Radio controlled irrigation systems require a license from the FCC.

Center line irritations have sprinkler locations down the center of the fairways. Twin-track are just that - lines down each side of the fairways.

Wall-to-wall usually means the roughs are also irrigated - sometimes with additional heads.

An average 18-hole irrigation system will have from 600 to 1,000 sprinkler heads. Individual sprinkle heads can cost from $60.00 to $120.00 or more a piece. The new self radio-controlled heads have been quoted as high as $900.00.

Check with the superintendent to find out how frequently the irrigation system needs repairs (secret: get a private meeting with the assistant superintendent if you really want the scoop). Check the spare parts inventory to see how well stocked it is. On the golf course you should look for blind spots indicating areas the sprinklers don't reach. Do all the sprinkler heads work? Did they cut any corners during installation? Does the system include fertigation tanks? When was the last time the main pump shaft was pulled and repaired (a $10,000 to $35,000 job).

In the USA and Canada, the most popular irrigation brands are Toro, Rain Bird, and Buckner. Beware of lesser name irrigation systems installed prior to 2000. Many are besieged with problems.

DRAINAGE

You must be certain that the drainage plan for the golf course is reliable, proper, and in good order. Get any and all documents and permits you need to satisfy yourself that these components are available now and forever. There are several drainage issues that will affect the course - and the business.

Anytime it rains, you'd like to know how long the course will be closed down (if at all). You should look for areas of erosion that will suggest poor drainage planning, or dried up puddle dimples in places indicating long-standing water. Check the sand traps to see how well they drain (most 10-year-old golf courses will have sand traps that won't drain and are in need of repair). Darker areas of sand traps will indicate possible drainage problems and sand mixing with native clay and soil.

CONSTRUCTION PLANS.

Get a copy of the subject golf course's construction plans. As new owner, you have no idea where the irrigation pipes and drainage pipes and tiles are located. I can tell you horror stories about drainage and irrigation systems.

ENVIRONMENTAL

Depending on where your target golf course is located, every county, every state (province) will have their own twist on environmental rules. Some will inspect your fuel bunkers with a magnifying glass, others don't even require a sealed fuel bunker, or double walled fuel tanks. Some agencies will transfer a storage license, others will require you to apply for a new one. Some won't require any fuel storage permits. It's a homework item.

Some states/counties/provinces may require a separate license for chemical storage. You can expect to be required to show a separate chemical storage room, or even a completely separate building. Full regulations require specific ventilation and proper shelving, etc., to be sure reactive chemicals are safely separated.

This will really get you, but if the property has natural ponds or waterways, you'll need to learn what (local) rules apply. Flora and fauna, wildlife, water quality, etc. may all be your responsibility maintained at your expense. A typical Florida golf course with acres of ponds and wetlands spends upwards of $20,000 a year for professional pond and wetland monitoring services. You'll need to review all the pond care documents to be certain they are fully conforming (I can tell you about disasters where the buyer did not do his homework).

If your target golf course is located in Ontario, Canada, and has a trout stream on the property, they guard it with tanks, guided missiles, and swat troops (just kidding). However, I'm sure you get my point. Do your homework. Find and review the documents!

THE CLUBHOUSE

The clubhouse is like any house except it sustains more wear and tear on a daily basis than an average home. On any given day, 200 golf players may walk in and out the front door. In my experience a golf course clubhouse ages about 20 times faster than an average residential home. Consider 200 golf player rounds a day for 100-days (as at a daily fee course in Chicago) and it's 20,000 times the clubhouse door swings on its hinges. If you went in and out of your house four times a day for over 13-years your household front door will swing about as many times as a clubhouse front door swings in 100 days. Clubhouses wear out fast.

"Plumbing will endure at least 200 flushes, plus all the drainage from kitchens and the cart washing areas. Consider 200 persons coming and going at least twice each day. A 40,000 thousand round golf course means a minimum of 80,000 entries and 80,000 exits from the clubhouse. Few clubhouses are constructed to endure that kind of traffic. It’s no wonder so many clubhouses look tired after only a few years! Anyway, the first thing your lender will want is an engineers report on the structural integrity of the building (your lender wants to see it). You need to check all the heating and cooling units, electrical supply, roof shingle condition (not usually an engineering issue), termite, plumbing, etc."

The layout of the clubhouse will be extremely important in how it encourages traffic, concession opportunities, and efficiency of operation (I'm your man for that study).

THE KITCHEN

Inspect the kitchen very carefully. You can learn a lot about how the place has been operated by the seller by the condition of the kitchen. But there are other important issues to consider too. Check the fire proofing system. All fire fighting extinguishers have tags that show the date of their inspections (you might ask a third party expert to inspect it). Make sure all the stoves are working 100%.

Ask about grease trap handling and cleaning. Ask about hood cleaning - frequency. Get the name of the company that cleans the fryer exhaust hood.

Check the coolers and freezers (ask a third party expert to inspect them). If they are more than five years old, expect major compressor repairs. Check around refrigerator doors and hinges for rust or cold air losses. Be sure to check the temperature gauges in coolers and refrigerators and beware if you cannot find them! Look at all the cooking utensils, dishes, serving equipment, and storage areas. These are extremely expensive items that can dry up your capital in a flash! Ask to see the local health unit’s inspection reports. Be sure that the health inspector has signed off all issues. You will also want a copy of the latest fire inspector’s report. If there hasn't been one lately, demand one. The building must be certified fire safety conforming or there's no deal, because the banker will not fund without it!

LOCKERS, SHOWERS, TOILETS

A 10-year-old clubhouse will show normal wear and tear, but neglect will accelerate deterioration. The smell of the locker rooms will tell you something about the seller's care. Check the tiles in the shower, look behind the toilets, flush each one, turn on the taps, flick the light switches, inspect the carpeting. Act like your planning to live in the clubhouse.

STORAGE SPACE

Too many clubhouses were designed without enough storage capacity. When you see stuff stored in hallways, or in traffic areas, you know you've got a storage problem. Every 10-year-old golf course has storage problems, so look to see if there are reasonable solutions available.

THE PRO SHOP

I look to see how the pro shop is located and designed to manage golfer traffic. The perfect scenario (I call a 10) is a pro shop where the cashiers can see the first and tenth tees, the parking lot and the practice range. Anything less is simply less, and more expensive and inefficient to operate.

In your inspection of the pro shop, do the white glove test around merchandise displays, behind the service counter, and in the golf professional's office. Check for old merchandise that's been there for a couple of years (you don't want to be paying invoice price for the old stuff). Ask to look at all the old tee sheets to see if they reflect the rounds reported in the seller's cash flow history.

POWER CARTS

Power cars are the single most profit-producing concession at golf courses today. However, they have a limited number of rounds on them before they hit redundancy. If the fleet is more than three years old (at a Florida course) it is ready to trade. If your research learns that carts are being towed in regularly, you know the fleet is about dead. Remember your credit information? You'll need it to lease or finance a cart fleet. (I have negotiated for several cart fleets from 50 to 135 cars by several makers: Club Car, E-Z-Go and Yamaha. Just another area where Mike Kahn and First Tampa Financial Group can help you.)

NEW: Batteries are now available in lithium-ion that charge quickly and run full-power until they quit. Before your next fleet, be sure to learn about advances in golf cart batteries.

Are they gasoline-powered carts? Are they electric powered carts? In our experience, golfers prefer electric cars. Electric cars are quieter and provide a smoother ride. However, hilly golf courses often need gas powered carts, because hill climbing drains energy from electrical powered carts reducing the number of holes per day they can run between eight-hour charges.

A golf cart is a motor vehicle. Check carts the way you might inspect a used car. Look at the tires, look at the upholstery, and check the brakes and steering. If it’s an electric cart, check the batteries. Do they match? Pull the caps to check the plates. Look for corrosion buildup. If it’s gas, start and stop several carts to be sure they are tuned properly. But I’ve got a better idea: Hire a golf cart service company to prepare you a report on the condition of the entire cart fleet. Some will do it for nothing if they think they’ll get the repair work!

Is the cart storage area in an efficient location? Carts stored more than a few feet from the clubhouse (pro shop) can be expensive to transport back and forth. While you're at it, check to see the condition of the electrical source. If you're not sure, have an electrician inspect the power source. With gas carts, check to see how they managed their gas consumption. How far do they need to take them to fill the gas tanks? These inefficiencies can be operational nightmares.

"I helped reorganize a cart fleet for a golf course and saved them over $20,000 a year in cart operation expenses. As a First Tampa Financial Group client, you get all this experience and know how working for you!" Mike Kahn

CART PATHS

The coverage and condition of the cart paths will have a bearing on cart life, as well as an impression on golfers (and the bankers). If the golf course is more than 10-years-old, you will have cart path repairs to consider. Check to see if they can be patched, or whether they need complete replacement? Replacing cart paths on an average 18-hole golf course can run from $100,000 to $200,000 or more. If you're not sure, get an estimate from a company that installs cart paths.

MAINTENANCE BUILDING AND OUTBUILDINGS

A modern maintenance building should be of no less than 5,000 square feet with an office, employee lunchroom, full service his and her washrooms with showers, and a spare parts room. If it is in the North Country (freeze zone) it should be heated (at least enough for a mechanic to work in the building off-season). It should be well ventilated. You need a high ceiling with at least three full height overhead doors. A mezzanine is extremely desirable for storage. Check for oil change areas, machine areas, hydraulic lifts, torches, welding equipment, air hose, water supply, electrical supply, and a reasonably sized yard. Check to see whether the more sophisticated machinery can be stored inside.

If the target golf course is more than ten years old, ask to view the 'graveyard' - where junk, old machinery and redundant equipment pile up. Sometimes these places can become environmental problems with old batteries, gas tanks, and oily engines, resting on the ground. (If burying dangerous or possibly polluting materials are suspected, require the seller sign an affidavit saying seller has not hidden any old equipment or chemicals on or 'in' the property.)

OUTBUILDINGS

The chemical storage shed (if they have one) should be ventilated and constructed according to local regulations. Check to see whether different chemical containers are stored apart from each other.

FUEL BUNKER

Most golf courses use gas and diesel fuel. Tanks larger than 50 gallons (or so) must be stored in a tightly sealed bunker. Some areas require poured concrete and sealed bunkers with no seams, and sides as high as three or more feet (enough to hold the contents of both fuel tanks). Other neighborhoods require only cement block structures with a sealer. Most will also require a concrete fueling platform to park vehicles for fuel.

UPDATE 2012: WASH STATION

Many states and counties now require golf courses to have special washing stations for mowing machine cleanup. For instance, a fully compliant wash station in Florida will be designed so that none of the water used to wash of reels and other mowing machines does not work its way back into the environment. A state-of-the-art wash station uses very little water by way of a recycling system of the same water while cleansing it. Grass and other materials than may contain fertilizers and other chemicals are safely separated for safe disposal. In 2011 I installed a system at a Florida golf course at a cost of $40,000 (approximately).

COMFORT STATIONS

Most golf courses today provide washrooms on the golf course (especially with so many women playing golf today). You'll learn a lot about the seller by the cleanliness of the comfort stations. If they are not well maintained, it's a negative reflection on earnings. Same as the clubhouse bathrooms. Flush the toilets, run the water, etc. Open and close the doors too.

RAIN SHELTERS

Good golf courses provide rain shelters. Just make sure they are safe and secure. Many have a perpetual urine smell. I wonder why?

GOLF COURSE

You're main interest is the golf course. There are eight basic components of a golf course:

1) Teeing grounds

2) Fairways

3) Greens

4) Rough areas

5) Bunkers

6) Natural hazards

7) Service center (clubhouse) and Infrastructure

8) Maintenance facility

In your interviews with the superintendent, you want to learn what grasses make up the tees, fairways, greens and rough areas. You'll be smart to look for Internet sites where you can become knowledgeable on the care and maintenance of the grasses on the target golf course. You should know that certain grasses on greens mutate over time and may need to be gutted and replaced. Understanding cutting heights, fertilizing programs, pest and weed controls will help you determine whether the seller has been keeping this work up (another effect on the cash flow statements). UPDATE 2013: I recently spoke with a Florida superintendent who told me his greens of only 12 years of age needed to be completely replaced. A private country club, they are trying to decide between the newer Bermuda types like Tiff Eagle, Champion Ultra Dwarf, or another grass known as seaside paspalum. Although the current greens were seemingly young, they were contaminated with common Bermuda grass and other unwanted plants. In my own diligence analysis of a golf course I want to know those things. Replacement for 18-greens and a practice green can run $100,000 for Champion to well over $200,000 for Eagle. Don't forget the lost revenue for at least four months adding to the real cost of replacing greens.

The condition of the tees will tell you one of two things. If they're worn out, they are too small, or the course is very busy. Always check the white tee boxes if you're trying to determine whether the place is busy or not. So few golfers play the back tees, they don't tell you anything. Always look at the white tee boxes.

You'll learn a lot about the maintenance program, and the efficiency of the irrigation and drainage system with your inspection of the fairways.

The same holds true for the greens and rough areas. You should also ask to view the superintendent's log books. These notes should indicate various fertilizing, chemical treatments, airification schedules, etc. They also may be required by law (or permit) to keep irrigation records. Have a look at them too. You can refer to your studies on care of the subject's grasses to see whether the seller has been keeping up with proper maintenance schedules. If not, reduce the earnings they show accordingly.

Inquire about the original construction of the greens. If they state they are USGA specifications (USGA Specs) greens, that means they are built the best way. UPDATE 2012: Greens built to USGA specifications are depreciable! Not many know that.

Go to http://www.usga.org/green/coned/greens/recommendations.html to review construction of USGA Spec greens. However, understand that most greens are not built to USGA specs.

The advantage of USGA Spec greens is in their drainage and how they promote deeper root growth - important in areas where water conservation is an issue. I can explain. Just write mike@golfmak.com.

We talked about the sand traps (bunkers) and how they appear. Sand depth should be a uniform two to three and one half inches and be the same color throughout the bunker area. If weeds and grasses are encroaching into the main sand areas, you're seeing another indication they are under-maintained - another deduction from earnings.

REVIEWING THE FINANCIAL STATEMENTS

Of course, you'll be interested in rounds played and financial information about the subject golf course. If numbers can fool or mislead, here's where you're going to see a lot of smoke and mirrors. Every seller wants to show you solid earnings and lots of potential to get the asking price for the property. However, as we indicate often above, earnings may be inflated by way of cutting corners in maintenance routines. The phrase, "pay me now, or pay me later!" applies here. In my experience, a golf course showing $500,000 a year in net earnings before taxes, depreciation, interest, and amortization is likely inflated by up to 20% or more (That's where I do my thing). I have a little joke about round counts...

"Every time a flock of birds fly over the first tee the owner counts them as rounds!"

NUMBERS THAT SHOULD CONCERN YOU!

The direction or trends for rounds and revenues are rather obvious when reviewing annual financial statements. Since 1997, just about every golf course in the USA is showing downward trends in rounds and income. I’m not worried about these trends for people who are buying golf courses for the long haul. That’s because I believe the downturn will level and recover sometime soon. UPDATE 2012: Golf's turnaround is not materializing as expected. In fact, player participation has declined steadily since 2000. Rounds are down from 2005 through 2011 almost everywhere. UPDATE 2013: We had a net loss of 154 golf courses in the USA in 2012. It is expected that we will lose at least that many in 2013. Nobody can really say what the golf-players-to-golf courses equilibrium is going to be as golfer age and leave by natural attrition. I see the industry is finally talking about the participation decline among themselves, but correction action is slow. It is my advice to any golf course buyer in 2013 (and beyond) to take a careful five to ten year forward look at the marketplace as part of diligence.

When studying the financial statements, you need to consider what your ‘working relationship’ with your golf course is going to be. That’s why I think you should look at department ratios to get a picture of the kind of business you are buying. Assuming your interest is to own and operate a golf course with yourself as day to day manager, it is important to make sure you're not getting yourself primarily into the food and beverage business. A golf course showing more than fifteen to twenty percent of its revenue from food and beverage sources can become an unpleasant experience, because the food department will consume most of your energy. Believe me, the food and beverage area of the golf course business is a number-1 pain in the butt if you’re depending on weddings and other outside functions for revenue. In my opinion, the energy required managing a full service F & B department is more than most people want. UPDATE 2013: I have watched so many new owners become distracted with the food and beverage business at the expenses of the golf course. I have always operated the food and beverage concession as an opportunity and nothing else. I have watched failure after failure when owners place too much energy, time and money in a part of a golf course that makes almost no money. The superintendent has a junk pile of machines and supplies, while the owner tries to serve the best steak in tow. My advice (in 2013) is to settle for a food concession that serves things that golfers want - sandwiches, fries, cold beer, soft drinks, etc. You don't need a chef. You don't need to please the 'mother of the bride', and if you mange your food concession like I do. My way makes money!

THERE'S UPSIDE IN THEM NUMBERS TOO

I'm a great believer in taking full advantage of my concession opportunities. I believe you’ll find ‘pockets of gold’ - especially if your diligence review indicates food and beverage at a course is losing money or pro shop merchandise profits show below, say, fifteen percent. In my opinion, as long as the food department represents less than fifteen percent of total revenues, and the pro shop indicates less than ten percent of revenues, you should not need a great deal of energy to make either of these concession opportunities profitable (I have formulas I use to form an opinion of the concession ‘energy-verses-opportunity’ issue). However, if the clubhouse is one of those 20,000 square foot monsters, I believe you'll have a never-ending problem!

EMPLOYEE REVIEW

You'll need to carefully study all employee documents and employee contracts. In some places (like Florida), all employees are released from employment at the moment the seller releases the property. It's great for a new owner, because you can interview them all and hire them as you see fit. You also have the opportunity to put forth your own employee policies. Obviously though, you'll want most of the rank and file employees to stay, unless you already have your replacement crew in place. Watch our for entitlements due employees like sick days and/or special bonuses that you might unknowingly inherit from the former owner.

THE CLOSING TABLE – BRING LOTS OF MONEY

The cost to close a golf course acquisition can be substantial. Consider that you will spend your own money (that you won't get back) in many areas to satisfy yourself (and the lender if you are borrowing from a bank) that what you see is what you get. An appraisal can cost up to $10,000. A survey will cost anywhere from $5,000 to $50,000. The finance source will charge up to 4 points, with up to $20,000 cash up front to start the loan application process. You'll pay for your own environmental survey, up to $3,000. A diligence guy like me gets $500.00 a day, plus expenses for up to 20 days of work (best money you’ll spend in the process). You'll have documentary stamps, legal expenses, transfer fees, utility deposits, license transfer fees, and more. You'll need cash for your new insurance policy, likely up to $10,000 down on an insurance policy. There will be an adjustment for you to take over remaining inventories in the pro shop (merchandise), kitchen and out in maintenance (fertilizer, chemicals, and supplies in stock). You'll likely have to buy all this stuff.

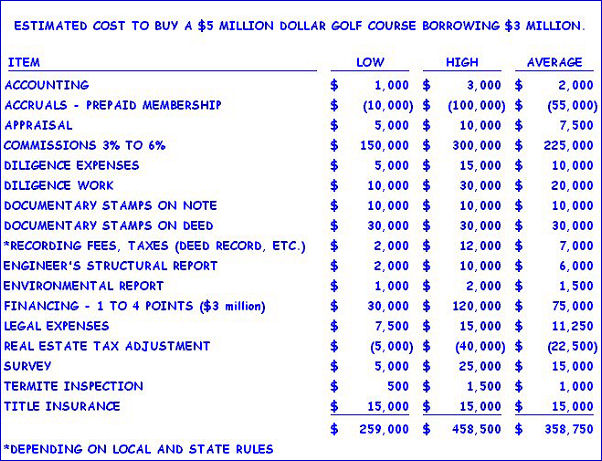

HERE'S WHAT IT REALLY CAN COST TO BUY A $5 MILLION DOLLAR GOLF COURSE AND OBTAINING A $3 MILLION DOLLAR MORTGAGE

GET OUT YOUR LEGAL PAD AND PENCIL AND START WRITING THIS STUFF DOWN

Unless you're paying cash for a property, your finance source wants several important assurances. You also must consider the effort, time and expense you'll be required to furnish a lender, such as:

1) Exactly what property is being transferred, evidenced by a survey (among other things)

2) An appraisal of the property by a certified property appraiser. It must be an appraiser approved by the lender (that kills having you cousin doing an inflated appraisal for you)

3) Evidence that the property has no adverse environmental issues

4) Engineers report on all permanent structures - clubhouse, outbuildings, etc.

5) Termite inspection and report

6) Title Search and Insurance

7) Agronomy Report. The best source is the United States Golf Association (USGA) http://www.usga.org/

8) Mike Kahn's Golf Course Property Review.

Remember, the seller is offering you the property on an as is basis, leaving you the effort and the cost of gathering the evidence you or your lender needs to be comfortable with what you're buying (and financing). Although some of these expenses may be negotiable between buyer and seller (seller may want a copy of your survey, which you can charge him/her for), otherwise, you can expect to pay these costs.

1) SURVEY - $5,000 TO $50,000, PLAN FOR TWO MONTHS TO COMPLETE A GOLF COURSE SURVEY

In a golf course transaction, the lender will want an updated survey of the property. All encumbrances, easements, environmental designations, drainage ditches, power lines, roadways and location of all improvements material to the property must be confirmed by the survey. Depending on the land configuration, surveyor's difficulty, and surveyor's fee structure, you can expect the cost to be anywhere from $5,000 to $50,000. Believe me, I ordered a survey for a golf course within 100's of acres of dense woods and gator infested swampland. The bill was over $50 thousand!

2) APPRAISAL - $5,000 TO $15,000, PLAN AT LEAST ONE MONTH

A golf course appraisal must be completed an appraiser party approved by the lender. Expect an appraisal to cost from $5,000 to $15,000. It's another item the seller, or a subsequent buyer may buy from you if you don't close - but don't count on it.

3) ENVIRONMENTAL 1, 2 OR 3 REPORT - $1,000 TO $50,000

Allow one month (these guys are very busy these days, so plan for at least two months in 2012) for an environmental 1 report, up to three months for an environmental 2 or 3 report. You and your lender want to be sure the property is not contaminated. Based on visual reviews and even rumors, the only one who doesn't want you to hear about contamination is the seller. I've heard of environmental cleanups in the $100's of thousands! In my opinion, many older golf courses (25 years or more) are almost sure to have at least some environmental issues - usually in the vicinity of the maintenance building - buried batteries, oil spills, or just continual dripping from the pouring spout from gas tank.

4) ENGINEER'S REPORT - $3,000 TO $10,000. ALLOW ONE MONTH

A lender will want an updated engineer's report on all permanent structures on the property. Clubhouse, maintenance building, pump house, etc. will need to be inspected by an approved engineer. You need to be careful with older clubhouses, as they can have problems that you inherit. Many older clubhouses non-conforming to 2002 standards - narrow doorways, staircases, no handicap ramps, etc. Watch out! Sometimes grand fathered non-conforming buildings can lose their status with a change of ownership - an issue your attorney wants to check carefully!

5) TERMITE INSPECTION - $500 TO $2,500 - ALLOW UP TO ONE MONTH

All permanent structures will require a termite inspection by an approved termite inspector. Cost will depend on the size and number of buildings to be inspected.

6) TITLE SEARCH AND INSURANCE - $ UP TO $15,000 FOR A $5 MILLION DOLLAR GOLF COURSE

You'll need to calculate the cost of title insurance. Even if you pay cash for the property you purchase, unless you are a very trusting person, you want the title insured for your own safety. However, a lender will require proof that a new title insurance policy takes affect upon transfer of the property. According to a web source, a $5 million dollar (Florida) golf course purchase will cost the buyer $15,000 for a title policy, plus title search expenses. (Is title insurance compulsory? Not by law, but if you're obtaining a mortgage, the lender will require it. Either way, the experts say don't do without it.)

7) AGRONOMY REPORT – UP TO $2,000, UP TO ONE MONTH FOR A REPORT

Best source for learning about greens, etc., the United States Golf Association Greens Section: http://www.usga.org/green/. It will pay you to order an agronomy report on the subject golf course – especially if the course is more than a dozen years old. An agronomist may find subtle problems like mutations and/or invading grasses you cannot detect yourself. Nematode problems and even inadequate maintenance practices or insufficient equipment may be identified in this report. The most important items required for this area of diligence is detective work and time (I was a golf course superintendent (my own). I know the issues.). A golf course purchase and sale contract should allow at least 60-days from signing to closing to allow for adequate diligence. With over 250 separate items to be reviewed and verified, including the lender's requirements, there should also be a clause included in the purchase contract allowing for a 'reasonable extension' should information implied by seller be delayed at no fault to you, as buyer.

8) GENERAL PROPERTY REVIEW

Before you make any decisions on a golf course, you should first order brief property review. You can save a lot of time and money from the initial information you gain from a quick property inspection and local market summary. You would hate to have thousands of dollars invested in a diligence program and find out negatives that would stop your when. BTW: That's one of my services. Don't forget: I might be the reason you don't buy that golf course!

DILIGENCE - $5,000 and UP - ALLOW TWO WEEKS

In a golf course purchase there are hundreds of details you, as buyer are wise to study. Based on the 'as-is' clause in the contract, it's up to you to know what you are getting. Unless you're are a seasoned golf course operator and have made these transactions before, you should engage an expert (like me) to assist you. I have the skill and experience to review the components that make up a golf course inside and out. I inspect and review maintenance equipment,irrigation system, cart paths, drainage issues, turf conditions, maintenance routines, and employee activities on the outside. On the inside I inspect the clubhouse, kitchens, pro shop, offices, locker rooms, washrooms, storage areas, etc. I see things other don't see! Things that will cost you a lot of money to repair or replace!

LEGAL - $5,000 TO $15,000

For a transaction as complicated as a golf course property, a Real Estate Attorney should be retained the moment an offer is planned. The attorney's job is to protect your legal rights and address the warrants and representations of the seller on your behalf. During the diligence period, the attorney's review of all pertinent legal documents, including the survey, and supervision of the closing statements is crucial to your protection. Remember that the lender will want an attorney's opinion as well.

ACCOUNTING - $1,000 TO $5,000

The lender may require an opening balance sheet prepared and delivered on a certified public accountant's letterhead. As an accounting source will be needed ongoing after the closing, selecting and retaining an accounting source should be done early in the diligence period. Best to find an accountant that understands golf course finances - maybe even handles golf courses. I've watched accounting fees escalate while the chosen accountant learns the business at the owners expense.

EXPENSES - UP TO $15,000

Expenses for the diligence party (like me), which includes travel, accommodation etc., will average approximately $150.00 a day over a 60 to 90-day period. A properly applied diligence effort will include intensive gathering and verifying of information about the subject property.

FEASIBILITY - $ PART OF YOUR DILIGENCE

We believe you should obtain a brief update on the current and future feasibility of the subject (which may be required by the lender anyway). However, we believe you should conduct your own in-house feasibility study for your own comfort. In our experience, a golf course market service area (MSA) changes over time. Populations shifts, new golf courses, etc., can dramatically affect demands for rounds of play at a golf course. The trend since 1997 had been a downward demand for rounds per golf course due to added competition (up 500 new courses a year in the USA from the early 1990's through 2004). You need to know where this trend is headed for the golf course named in your purchase and sale contract. You need to know the neighborhood.

"I am an experienced golf course expert with over fifty years in the golf business. I conduct localized feasibility studies, and prepare business plans and pro forma for golf course buyers applying for financing. When I work with you as your Buyer’s Agent, you have me in your corner all the way. I can help match you or your company with an appropriate golf course, assist in preparing and presenting a contract, assist in procuring financing, complete the diligence, and finally, supervise the ownership transition."

BUSINESS PLAN - $4,000, OR INCORPORATED WITHIN THE/A DILIGENCE CONTRACT

The lender will want a business plan showing how the buyer plans to operate the property going forward. The plan must include an executive summary, operation plans, marketing plans, improvement plans, and pro forma statements for one-year and five-years. Be prepared to defend every line of your pro forma, as some lenders will isolate every penny mentioned in your business plan.

PROPERTY SURVEILLANCE ANALYSIS AND REVIEW - $2,500 OR PART OF THE/A DILIGENCE CONTRACT

Under a Purchase and Sale Contract you have the right of inspection of the books and records of the subject property. You'll review membership lists, supplier lists, employee list, all contracts, permits, licenses and agreements. You'll review all documents and lists of personal property to be conveyed via estoppel agreement. You'll review all inventories, equipment, and machinery, etc. Your review work will include visits to government offices to review permits, land use permits, fuel storage licenses, food service permits, drainage permits, irrigation permits, and any government-controlled activity for the property.

Diligence must uncover any and all previous and pending lawsuits, liens, property work orders, or any documents that may cloud either title, or buyer's ability to conduct business without interference after the close.

FINANCE FEES/POINTS - $30,000 to $120,000 ($3 MILLION BORROWED).